A business is a living, breathing system—shaped by its past owners, swayed by market forces, and bound by economic realities like interest rates, inflation, and regulatory policies. Yet, despite these shifting dynamics lies a fundamental truth: business ownership remains one of the most effective paths to wealth creation.

In Main Street Millionaire: How to Make Extraordinary Wealth Buying Ordinary Businesses, Codie Sanchez challenges the idea that business ownership should be reserved for Wall Street elites. She shifts the focus to Main Street—the small, local businesses that quietly generate $6.5 trillion in annual revenue in the U.S.

Laundromats, plumbing services, car washes, coffee shops—businesses that are often dismissed as unglamorous but are, in reality, the backbone of the economy. Unlike the towering corporations of Wall Street or the stable, mid-sized firms of the middle market, Main Street businesses tend to be smaller, more owner-dependent, and sometimes lack pristine financial documentation.

This makes them riskier in the eyes of traditional investors. But risk, when understood properly, creates opportunity. For immigrant entrepreneurs willing to look past the hype of trendier sectors, these businesses present a unique chance to build generational wealth—especially now, as a wave of aging owners prepares to retire.

But recognizing a great opportunity is only half the battle. After defining the right business to buy (as we explored in our What to Consider Before Buying a Business series), one daunting question remains: How do I pay for it?

For many immigrant entrepreneurs, securing financing is the toughest hurdle. Limited local credit history, unfamiliar financial systems, and risk-averse lenders create a financing wall that can feel impossible to scale. The paradox is frustrating: you need a business to establish financial credibility, but financial credibility is often a prerequisite to owning a business.

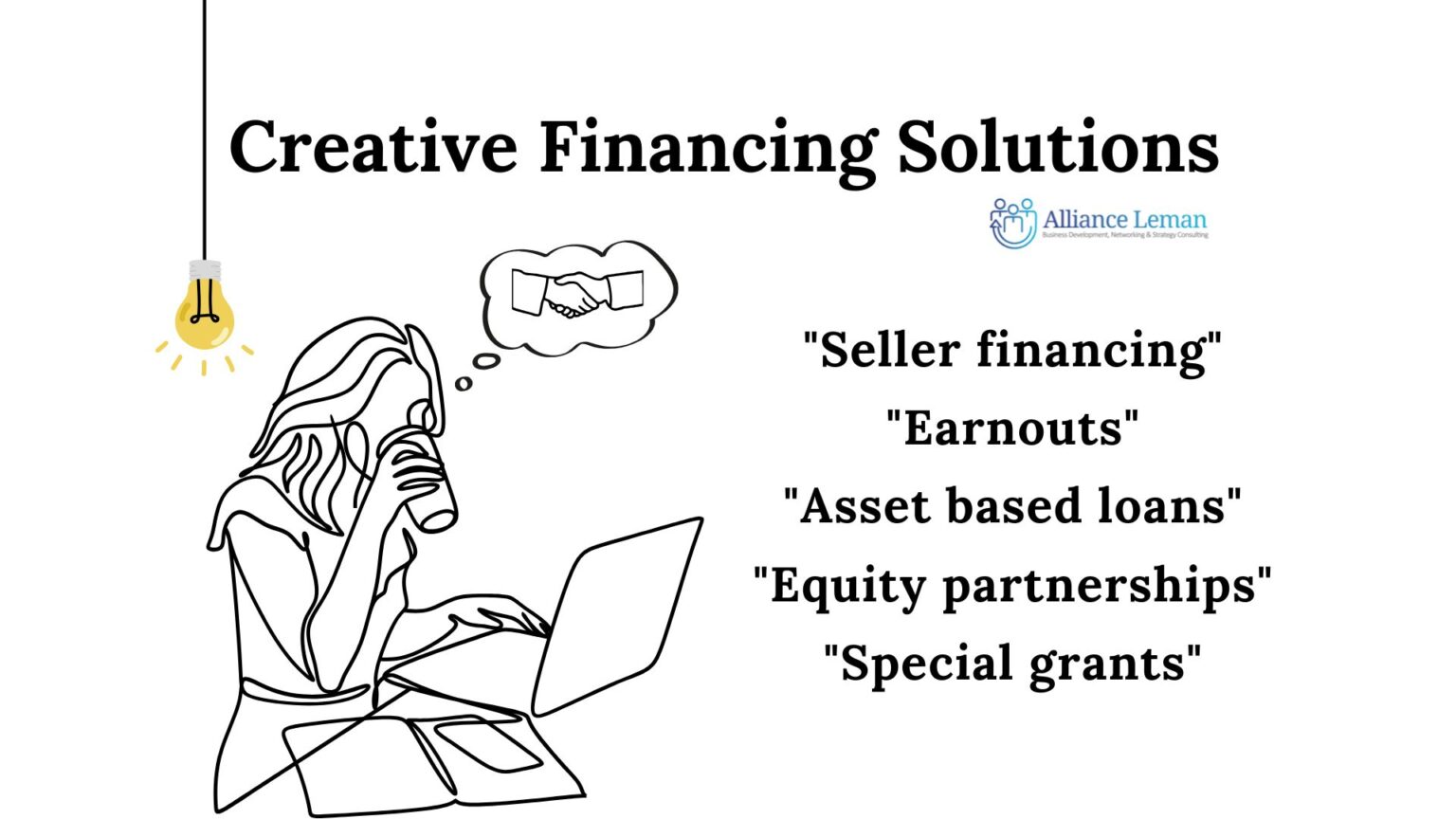

So, what happens when traditional doors—bank loans, personal savings, investor-backed funding—remain firmly shut? This is where creative financing becomes a game-changer.

While traditional M&A deals rely on cash payments and bank loans, alternative methods like seller financing, earnouts, equity partnerships, and asset-based lending can bridge the gap between buyer and seller expectations. These strategies aren’t just theoretical—they are actively shaping both large-scale acquisitions and smaller Main Street deals.

In this article, we’ll explore how aspiring immigrant business owners can leverage these creative financing techniques to turn ambition into ownership—without being blocked by traditional financial barriers.

Let’s dive in.